Search Knowledge Base by Keyword

Avoiding or Reducing Self-Employment SE Taxes

By Jason Watson, CPA

By Jason Watson, CPA

Posted Monday, October 23, 2023

A common complaint from those who own their own business is self-employment tax. Can you avoid, reduce, eliminate or lower your self-employment taxes or SE taxes? Ok, we just said two things that mean the same thing twice. Yes, you may reduce self-employment taxes to a large extent, but it takes some effort starting with an S Corp election (let’s not get ahead of ourselves yet).

If you own a business as a sole proprietor or as a garden variety single-member LLC (one owner or member) your business income will be reported on your personal tax return under Schedule C and is subject to self-employment tax (currently 15.3%) and ordinary income tax. So, you could easily pay an average of 40% (15.3% in SE taxes + 24% in income taxes) on all your net business income in federal taxes. Wow, that sucks!

A similar taxation exists for partnerships / multi-member LLCs too since the issuing K-1 will identify the income subjected to self-employment taxes (and of course income taxes, just like the example above).

The “double” taxation should not be a stranger to you. When you were paid a W-2 salary of wage, you had Social Security and Medicare taxes taken out of your paycheck, and you also had income taxes withheld based on some payroll table. Only income taxes were “negotiated” by deductions and credits; Social Security and Medicare taxes were not.

Back to the sole proprietors and LLCs. We are all humans, and we generally spend what we make. If you are not prepared for 30% to 40% in taxes for your business income, it could be a shocker on April 15.

The recent tax reform and specifically the pass-through taxation changes in Section 199A do not alter the theory of self-employment tax savings. The additional pass-through deduction afforded to small business owners complements the benefits of an S corporation. Please bear with us as we go through the mechanics of saving self-employment taxes with an S Corp.

How Self Employment Tax Is Computed

A bit of disclosure is in order. Self-employment taxes are 15.3% which is derived from the “employer” portion at 7.65% and the “employee” portion of 7.65%. However, a small business gets to deduct its portion of payroll taxes from income before determining the taxable income. Huh?

Think of your last job where you received a W-2. The employer might have paid you $100,000 and withheld your portion of Social Security and Medicare taxes on your behalf. The business also had to pay its portion of Social Security and Medicare taxes, so its total expense was the $100,000 salary plus $7,650. Similar concept with sole proprietorships and LLCs.

Here is an illustrative table-

| Net Business Income | 100,000 |

| less SE Tax Adjustment at 7.65% | 7,650 |

| Taxable Business Income | 92,350 |

| SE Tax at 15.3% | 14,130 |

| Tax Deductible Portion | 7,065 |

Do you see the $14,130 or 14.13% of $100,000? That is essentially your effective rate of tax on self-employed business income because of the deductible portion of 7.65%. Probably doesn’t make you feel any better but there you go.

Quick Analysis of S Corp Savings

If you own a business and have elected to be treated as an S Corp (Subchapter S) for taxation, the business now files a corporate tax return on Form 1120S. We will detail this out with a fancy graphic, but basically an S corporation chops up the net economic benefit to the owner between salary and net ordinary business income after expenses and deductions. This split is important. Why?

The salary is subjected to Social Security and Medicare taxes; the net ordinary business income is not. The salary is paid to the employee (you). The net ordinary business income may be paid to the investor (also you). You’ll see several references to this concept that as an S corporation owner you are both employee and investor.

Let’s look at some quick numbers. These are based on using a salary of 40% of net ordinary business income after expenses and deductions for amounts up to $500,000 and then decreased incrementally to 30% for the millionaire at $2,500,000 below (real case actually). The 40% / 30% is for illustration (we will discuss reasonable shareholder salary in silly detail in a later chapter dedicated to only reasonable salary determinations).

Here is our summary table-

| Income | Total SE Tax | Salary | Total Payroll Tax | Savings $$ | Delta % |

| 30,000 | 4,239 | 12,000 | 1,836 | 2,403 | 8.0% |

| 50,000 | 7,065 | 20,000 | 3,060 | 4,005 | 8.0% |

| 75,000 | 10,597 | 30,000 | 4,590 | 6,007 | 8.0% |

| 100,000 | 14,130 | 40,000 | 6,120 | 8,010 | 8.0% |

| 150,000 | 18,711 | 60,000 | 9,180 | 9,531 | 6.4% |

| 200,000 | 20,050 | 80,000 | 12,240 | 7,810 | 3.9% |

| 300,000 | 22,972 | 120,000 | 18,174 | 4,798 | 1.6% |

| 500,000 | 29,991 | 200,000 | 20,494 | 9,497 | 1.9% |

| 750,000 | 38,764 | 262,500 | 22,307 | 16,457 | 2.2% |

| 1,000,000 | 47,537 | 350,000 | 24,844 | 22,693 | 2.3% |

| 2,000,000 | 82,630 | 600,000 | 32,094 | 50,536 | 2.5% |

| 2,500,000 | 100,177 | 750,000 | 36,444 | 63,733 | 2.5% |

Chart Notes

Let’s review some interesting things about the data on the previous page.

The bulk of payroll taxes are Social Security and Medicare taxes, which are combined to be called FICA taxes when payroll specialists are kicking it around the water cooler. You might have other payroll taxes such as unemployment (Yes, some states require it even for one-person corporations) and state disability insurance (SDI).

As mentioned, salaries started at 40% through $500,000 and then reduced to 30% at $2M and $2.5M. This is a jumping-off point. The IRS standard is “reasonable shareholder salary” which includes all sorts of non-qualitative things such as your expertise, Bureau of Labor Statistics, comparison of salary to distributions, zodiac sign, favorite color, etc.

Social Security taxes of 12.4% stop at $168,600 (for the 2024 tax year) of net ordinary business income for LLCs and partnerships who do not elect S corporation status. It also stops at $168,600 for salaries.

Medicare taxes of 2.9% continues into perpetuity. Not only does this go on into perpetuity, it also goes on forever (yes, that is supposed to be a joke). This is one of the major components of savings in the upper incomes since Medicare taxes are capped at the amount of salary with S Corps. In other words, if you earn $1M you will pay Medicare taxes on the entire net ordinary business income, but if you elect S Corp status and pay yourself a $400,000 salary you only pay Medicare taxes on the $400,000.

The Medicare surtax starts for those earning $200,000 and filing single, and $250,000 for those filing jointly. This too continues into perpetuity for LLCs and partnerships. In the data, we assumed a joint tax return. For example, at $500,000 net ordinary business income there is a $1,906 Medicare surtax. But if this business elects S corporation taxation and pays $200,000 salary, there is not a Medicare surtax. There is not a net investment income (NII) tax on the S corporation ordinary income either (more on that loophole later) since you materially participate; in other words, your investment into your S Corp is not passive.

Savings as a percentage of income starts to drop off at $168,600 which makes sense given the Social Security cap for the 2024 tax year. And those savings bottom out around $300,000 net business income and then begin a decent climb rate. Without getting into excruciating details and mental gymnastics, there is an interesting dynamic at $300,000 between Medicare taxes including the surtax on the LLC / partnership income, the salary being paid within an S Corp election, and Medicare taxes associated with that salary.

The Source of the Savings

The S Corp election of your Partnership, LLC or C corporation changes how the business reports income to the IRS. An S Corp prepares and files a Form 1120S which is a corporate tax return. That in turn generates a K-1 for each shareholder. Remember, shareholder, investor and owner are synonymous terms for our discussions.

This might be your first brush with the term K-1. A K-1 is similar to a W-2 since it reports income and other items for each member, partner, shareholder, owner or beneficiary, and is coded to tell the IRS how the business activities should be treated.

A K-1 is generated by an entity since the entity is passing along the income tax obligation to the K-1 recipient (hence the concept pass-through entity, or PTE for TLA lovers). There are three basic sources for a K-1, and the source dictates how the income and other items on the K-1 are handled on your individual tax return (Form 1040). Here they are-

- Partnership / MMLLC (Form 1065)

- S Corporation (Form 1120S), and

- Estate or Trust (Form 1041)

There are two types of K-1s for the purposes of our self-employment tax conversation- one is generated from a partnership tax return and the other is generated from an S corporation tax return. These K-1s look nearly identical and both are reported on page 2 of Schedule E in conjunction with your Form 1040. Schedule E is the tax form used for rental properties, royalties and other investment income including business income from a partnership or an S Corp.

However, a K-1 generated from a partnership tax return which has ordinary business income in box 1 and / or guaranteed payments in box 4 will typically be subjected to self-employment taxes for an active partner or member. Conversely, ordinary business income in box 1 on a K-1 from an S corporation will not be taxed with self-employment taxes. The S corporation election changes the color of money (we love this saying).

Note: S Corps do not have guaranteed payments like partnerships might- S Corps would call these payments wages or salary. A partnership (and an LLC for that matter) cannot pay its partners or owners a wage or salary. The IRS frowns on this. Any periodic payment that is recurring in a partnership to one of the partners is called a guaranteed payment and is reported separately from partnership income. Both might be subjected to self-employment taxes.

You just heard the term “pass-through entity” and you might also hear the term “disregarded entity”- a disregarded entity is a single-member LLC. As the terms suggests, it is disregarded for tax purposes, and therefore does not have to file its own tax return since the taxable consequence is reported on the owner(s) individual tax returns (Form 1040) as a sole proprietorship (Schedule C).

A pass-through entity passes its federal tax obligation onto the partner of a partnership, the member of an LLC, the shareholder of an S corporation or the beneficiary of an estate or trust. States might impose a business tax or a franchise tax on the partnership, LLC or S Corp directly (they legally cannot impose an income tax… more about interstate commerce rules later).

Quick Recap, The S Corp Money Trail

So, when your partnership, LLC or corporation is taxed as an S Corp you are considered both an employee and a shareholder (think investor). As an employee being paid a salary, your income is subjected to all the usual taxes that you would see on a paystub- Federal taxes, state taxes, Social Security taxes, Medicare taxes, unemployment and disability.

However, as a shareholder or investor, you are simply getting a return on your investment. That income, as the Romneys, Gates and Buffets of the world enjoy, is a form of investment income and therefore is not subjected to self-employment taxes (tiny exception for income over $200,000 (single) or $250,000 (married) where Medicare surtax is charged).

As you recall, when we say self-employment taxes, we are really talking about Social Security and Medicare taxes. From a sole proprietor perspective, they are self-employment taxes. From an employee perspective, they are Social Security and Medicare taxes. Same thing.

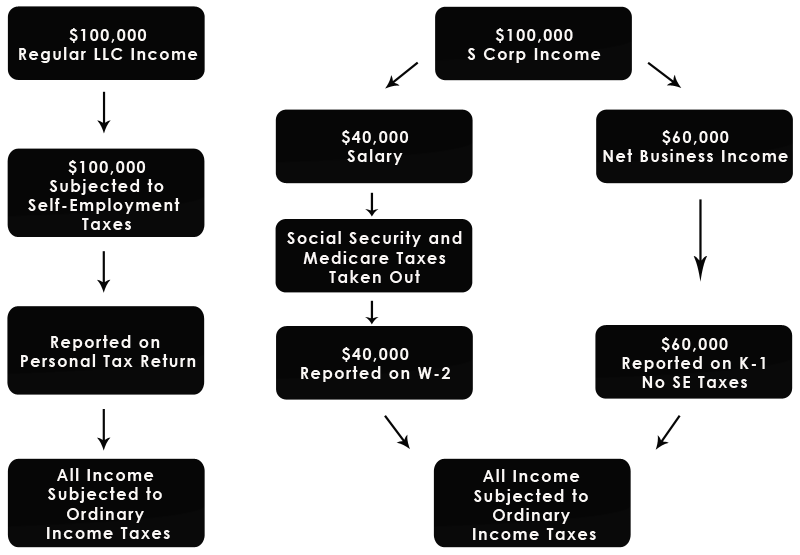

Let’s look at another visual in terms of how the money travels-

The four boxes on the left is the money trail of your sole proprietorship, LLC or partnership. The series of boxes on the right is the money trail of your entity being taxed as an S corporation. Note the $60,000 chunk of income on the far right hand side that is not being taxed at the self-employment tax level. This is the source of your savings.

The four boxes on the left is the money trail of your sole proprietorship, LLC or partnership. The series of boxes on the right is the money trail of your entity being taxed as an S corporation. Note the $60,000 chunk of income on the far right hand side that is not being taxed at the self-employment tax level. This is the source of your savings.

Also note that all your $100,000 is being subjected to income taxes. This is a common misconception- a lot of business owners believe there is a magical income tax reduction with an S Corp election. Not true. The only reduction is in self-employment taxes. All other tax deductions such as operating expenses, home office expense, mileage, meals, 401k plans, etc. are equally deductible with or without an S corporation.

Still not sure or not convinced? No problem… please check out Line 4 on Schedule 2 on your 2022 Form 1040 tax return. This number reflects the self-employment taxes paid on your business income.

We want to reduce this by 60 to 65%. If you see $15,000 then we can save $9,000 ($15,000 x 60%). This makes sense right? $100,000 in biz income would be $15,000. 8 to 10% of $100,000 is $9,000.

The previous table showed significant savings using a 40% salary without self-employed health insurance (SEHI). Again, we are only focused on the self-employment tax and payroll tax savings at this point. Section 199A from the Tax Cuts & Jobs Act of 2017 will be wormed into overall tax savings in a later chapter dedicated to qualified business income deduction. While reducing overall taxes and leveraging the pass-through tax deduction cannot be ignored, we are isolating payroll taxes to drive home a critical point.

Multiple Owners Savings

We have been discussing a one-person band in terms of savings and the flow of money. However, let’s briefly chat about the killer savings for a more than one owner situation. If the business had net ordinary business income after expenses and deductions of $150,000, and was split down the middle, each owner (two in this example) would pay nearly $7,000 in unnecessary self-employment taxes or $14,000 combined. A big number for sure, but consider the following.

WCG recently had a 9-person consulting firm being taxed as a partnership where each member earned about $125,000. The before and after analysis yielded a savings of just over $100,000 combined. Our fee for the S Corp administration (Vail Business Advisory Service) plus all the tax returns and tax planning was about $14,000 or approximately $1,550 per owner. And each owner saved about $12,000 in taxes and therefore pocketed $10,000 each.

The super sad part of this is that this entity was in place for over a decade with similar income and owners. Over a million dollars was wasted in unnecessary taxes. When you look at it that way, it makes you gulp a bit.

What happens when the business pays for your health insurance? Let’s find out how this can really soup up your tax savings.

Jason Watson, CPA, is a Senior Partner of WCG CPAs & Advisors, a boutique yet progressive tax,

accounting and business consultation firm located in Colorado serving clients worldwide.![]()

![]()

Taxpayer's Comprehensive Guide to LLCs and S Corps 2023-2024 Edition

This KB article is an excerpt from our 400+ page book (some picture pages, but no scatch and sniff) which is available in paperback from Amazon, as an eBook for Kindle and as a PDF from ClickBank. We used to publish with iTunes and Nook, but keeping up with two different formats was brutal. You can cruise through these KB articles online, click on the fancy buttons below or visit our webpage which provides more information at-

|

|

|

| $59.95 | $49.95 | $39.95 |

Taxpayer's Comprehensive Guide to LLCs and S Corps 2023-2024 Edition