Search Knowledge Base by Keyword

Controlled Groups

By Jason Watson, CPA

Posted Saturday, November 5, 2023

Another concern is controlled groups. If you think you are clever and create a holding company to only offer retirement savings plans to certain employees (like your family), the IRS says No. There are controlled group rules where a holding company that controls another business must offer the same retirement programs for both businesses.

Two general types of controlled groups might exist- a parent-child and brother-sister. The parent-child is where one business owns another. That’s simple. It gets a bit more complicated with brother-sister where various individuals own multiple businesses. By definition, a brother-sister controlled group exists when five or fewer individuals, estates or trusts own a controlling interest (80% or more) in each organization and have effective control.

Two general types of controlled groups might exist- a parent-child and brother-sister. The parent-child is where one business owns another. That’s simple. It gets a bit more complicated with brother-sister where various individuals own multiple businesses. By definition, a brother-sister controlled group exists when five or fewer individuals, estates or trusts own a controlling interest (80% or more) in each organization and have effective control.

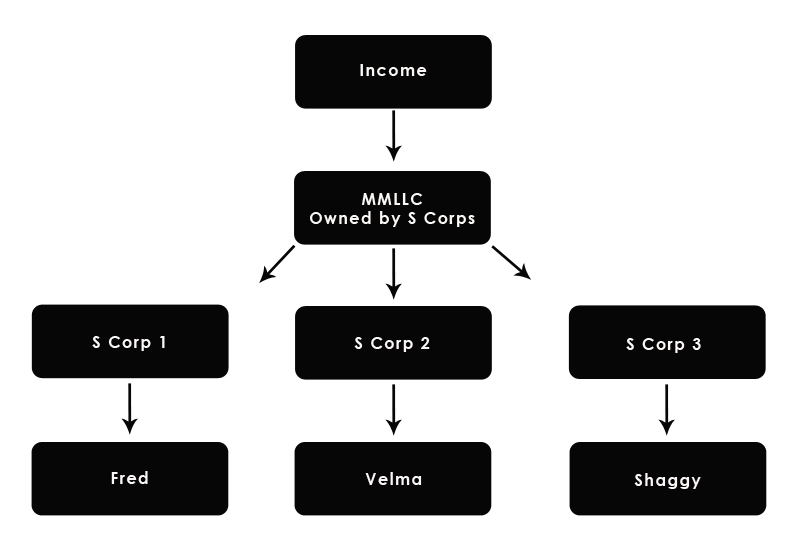

For example, you are smart and you connect with two other smart people to form a multi-member LLC. Since you have a revenue splitting scheme that varies from year to year, you use the multi-member LLC as a funnel and feed income to the underlying S corporations. Therefore, each person owns an S Corp that owns an equal interest in the multi-member LLC. Simple enough.

In this example, a 401k plan would be better implemented at the multi-member LLC level. Let’s dive into the details shall we?

Affiliated Service Group Rules

Let’s say a law firm is structured as a partnership similar to the schematic above. There are three partners. Each partner is separately incorporated as a professional corporation and taxed as an S Corp. Each corporation has a one-third partnership interest in the law firm (MMLLC). The sole employee and sole shareholder of each professional corporation is an attorney who would otherwise be an individual partner of the law firm if he or she were not incorporated. Easy so far.

All billings for legal services are done by the law firm and partnership income is distributed among the corporate partners according to the Operating Agreement. The law firm is the First Service Organization (FSO) and each of the three S corporations is an A-Organization (A-Org) with respect to that FSO. The four organizations constitute an Affiliated Service Group (ASG). This is the “classic example” of an ASG and can create all kinds of problems with retirement plans.

How did we go from easy to yuck in just a few sentences? A business is automatically a First Service Organization (FSO) if it engages in one of the following fields-

- Accounting

- Actuarial Science

- Consulting

- Engineering / Architecture

- Health / Medicine

- Insurance

- Law

- Performing Arts

This list should look a little familiar; it was the basis for the specified service trade or business (SSTB) designations for Section 199A. While you do not see certain professions called out, such as Financial Advisors, the IRS and ERISA are more concerned with function over form. Accounting + Consulting + Insurance might equal Financial Advisor. So be careful on trying to consider this list to be strict from a definitions perspective.

If you are an ASG, then the employees of all of the ASG businesses are deemed to be employed by a single employer for purposes of meeting the retirement plan provisions outlined below-

- Non-discrimination rules, IRC Section 401(a)(4)

- ADP/ACP testing for 401k plans, IRC Sections 401(k) and 401(m)

- Compensation limits, IRC Section 401(a)(17)

- Participation and coverage rules, IRC Sections 401(a)(3), 401(a)(26) and 410

- Vesting rules, IRC Sections 401(a)(7), and 411

- Limits on contributions and benefits, IRC Sections 401(a)(16) and 415

- Top-heavy rules, IRC Section 416

- SEP and SIMPLE rules, IRC Sections 408(k) and 408(p)

How do the IRS and ERISA find out? Challenging for sure! We’ve seen businesses run around with an ASG for a decade without a problem. But let’s say the IRS develops an app that allows them to peer over your shoulder. Aside from them telling you to floss more, they also notice your 401k plan.

Jason Watson, CPA, is a Senior Partner of WCG CPAs & Advisors, a boutique yet progressive tax,

accounting and business consultation firm located in Colorado serving clients worldwide.![]()

![]()

Taxpayer's Comprehensive Guide to LLCs and S Corps 2023-2024 Edition

This KB article is an excerpt from our 400+ page book (some picture pages, but no scatch and sniff) which is available in paperback from Amazon, as an eBook for Kindle and as a PDF from ClickBank. We used to publish with iTunes and Nook, but keeping up with two different formats was brutal. You can cruise through these KB articles online, click on the fancy buttons below or visit our webpage which provides more information at-

|

|

|

| $59.95 | $49.95 | $39.95 |

Taxpayer's Comprehensive Guide to LLCs and S Corps 2023-2024 Edition