Search Knowledge Base by Keyword

Medical C Corp

By Jason Watson, CPA

By Jason Watson, CPA

Posted Saturday, October 21, 2023

One the many challenges facing small business owners is health insurance and out-of-pocket medical bills. Generally speaking, self-employed health insurance premiums, including dental and vision, are directly paid by the business and are deducted as Officer Compensation on a business tax return That’s good. Health Savings Account (HSA) contributions are also directly paid by the business and are deducted as Officer Compensation. More good news!

As we stated elsewhere, these fringe benefits inflate Officer Compensation but are later deducted on the owners’ individual tax returns. We call this an “in and out” since the net change on the individual tax return is zero and the actual deduction takes place on the business tax return. But what about out-of-pocket medical expenses like co-pays, lab fees, prescriptions, etc.?

Health Reimbursement Arrangements (HRA) have been around since the 1960s and became very popular in the 1990s, but they recently went through a transformation as a result of the Affordable Care Act. The 21st Century Cures Act and H.R. 34 established the Qualified Small Employer HRA (QSEHRA, pronounced “Q Sarah” opposite of “Suzie Q”). Beginning in 2017, qualified businesses with fewer than 50 employees who did not offer group health plans could use a QSEHRA to reimburse for health insurance premiums and out-of-pocket medical expenses.

There is a catch! A greater than 2% shareholder of an S corporation cannot participate in a QSEHRA. They can, however, participate in a garden variety Section 105 HRA but still do not enjoy the income tax deduction of HRA reimbursements. Huh? If an S Corp reimburses a shareholder, that amount is added to Box 1 of the W-2 as Officer Compensation just like self-employed health insurance premiums and HSA contributions. The huge difference is that HRA reimbursements are not later deducted on the owners’ individual tax returns as they are with self-employed health insurance premiums and HSA contributions. Instead, they are reported on Schedule A as medical expenses subject to all the usual limitations.

There is still a savings however! As we will reiterate many times throughout the book, self-employed health insurance, HSA contributions and HRA reimbursements can be leveraged into providing a lower yet reasonable S Corp shareholder salary.

Let’s assume that data support an $80,000 Officer Compensation as reasonable.

| Officer Compensation | 80,000 | |

| less Self-Employed Health Insurance | 10,700 | |

| less Health Savings Account | 8,300 | max for 2024 |

| less Health Reimbursement Arrangement | 10,000 | |

| Salary Needed to be Paid | 51,000 |

As you can see, we are “building” Officer Compensation by adding wages, health insurance, HSA and HRA components together. How does this help?

Here is a quick table that illustrates how leveraging the non-salary components of Officer Compensation reduces Social Security and Medicare taxes-

| Box 1 (Wages Subject to Income Tax) | 80,000 |

| Box 3 (Wages Subject to Social Security Tax) | 51,000 |

| Box 5 (Wages Subject to Medicare Tax) | 51,000 |

| Total Social Security and Medicare Taxes Saved | 4,437 |

Recall that earlier we determined $80,000 was considered a reasonable amount of Officer Compensation (of course, yours will vary). But because of other components, we were able to pay a salary of only $51,000. This $29,000 reduction in salary saved $4,437 in Social Security and Medicare taxes. In the absence of other components, we would have had to pay $80,000 in wages. Yuck.

Back to the HRA. In our example, the S Corp reimbursed $10,000 in out-of-pocket medical expenses. Unlike self-employed health insurance and HSA contributions, there is not an income tax savings, but there is a Social Security and Medicare tax savings as you see above. Specifically, $10,000 x 15.3% or $1,530 was saved by having an HRA.

TASC charges $600 for HRA plan administration (2021 rates). As such, an HRA in this example put a $1,000 in your pocket. Not too shabby for very little effort.

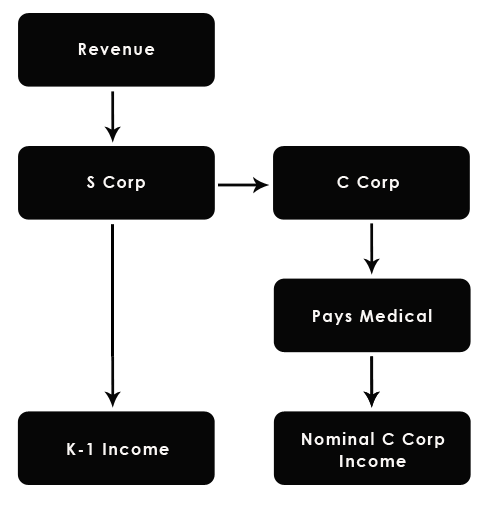

How could we get an income tax deduction using an HRA? Good question. That is where a C corporation comes into play.

A C Corp is not a pass-through entity and therefore it does not have to worry about the greater than 2% shareholder rules that S Corps face. Therefore, a small business owner could set up a C Corp that offers services to an S Corp in a business to business transaction (such as a fee for service agreement), and then pays medical bills on behalf of the C Corp employee(s). The S Corp’s income would naturally be reduced by the fees paid to the C Corp which would have a double benefit; lower income taxes and a possibly reduced shareholder salary.

You would need a business purpose for the C corporation such as providing marketing or management services. To buttress this, you could identify certain expenses to be paid from the C Corp. For example, you would pay for web hosting, SEO services and other marketing expenses from the C corporation, plus the medical expenses.

The savings might be significant. TASC boasts a 20% add-on to your marginal tax rate; this 20% seemingly represents the Social Security, Medicare and state income tax savings added to your federal marginal income tax rate. We don’t necessarily agree since the Social Security and Medicare component is already available with an HRA deployed in a standalone S corporation. But… if we play along… if you spent $10,000 in out-of-pocket medical expenses at a combined marginal tax rate of 30% (24% + 6% for state), then you save $3,000 by using the C corporation entity structure. An additional tax return would be required at around $1,000 in tax preparation fees so you pocket $2,000.

If you have $20,000 in annual medical expenses, then your savings would be $6,000. Those are real dollars.

What about audits? C Corps with under $250,000 in assets have a 0.5% audit rate and S Corps have a 0.4% audit rate. Individual tax returns with a small business are upwards to 2%, and even higher with travel, meals and auto expenses (the low hanging IRS fruit). As a side note, if your C corporation has $20B in assets you audit rate in 2017 was 58%. Luckily most people reading this book are about $20B away from having to worry.

More discussion is required to ensure the C Corp idea fits your objectives, but you can see the basic arrangement.

Jason Watson, CPA, is a Senior Partner of WCG CPAs & Advisors, a boutique yet progressive tax,

accounting and business consultation firm located in Colorado serving clients worldwide.![]()

![]()

Taxpayer's Comprehensive Guide to LLCs and S Corps 2023-2024 Edition

This KB article is an excerpt from our 400+ page book (some picture pages, but no scatch and sniff) which is available in paperback from Amazon, as an eBook for Kindle and as a PDF from ClickBank. We used to publish with iTunes and Nook, but keeping up with two different formats was brutal. You can cruise through these KB articles online, click on the fancy buttons below or visit our webpage which provides more information at-

|

|

|

| $59.95 | $49.95 | $39.95 |

Taxpayer's Comprehensive Guide to LLCs and S Corps 2023-2024 Edition